1. Introduction

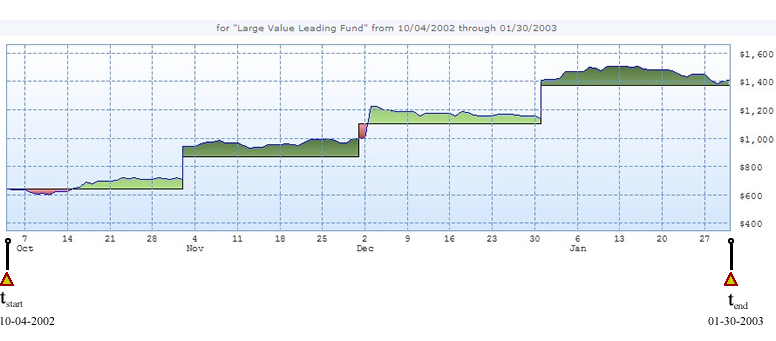

In this section we show how to connect performance measurement concepts to actual returns using real cashflows. Here, we will calculate a return using the "Time-Weighted Rate of Return, Daily Valuation" method for one hypothetical holding, the "Large Value Fund" for the period 10/04/2002 through 01/30/2003.

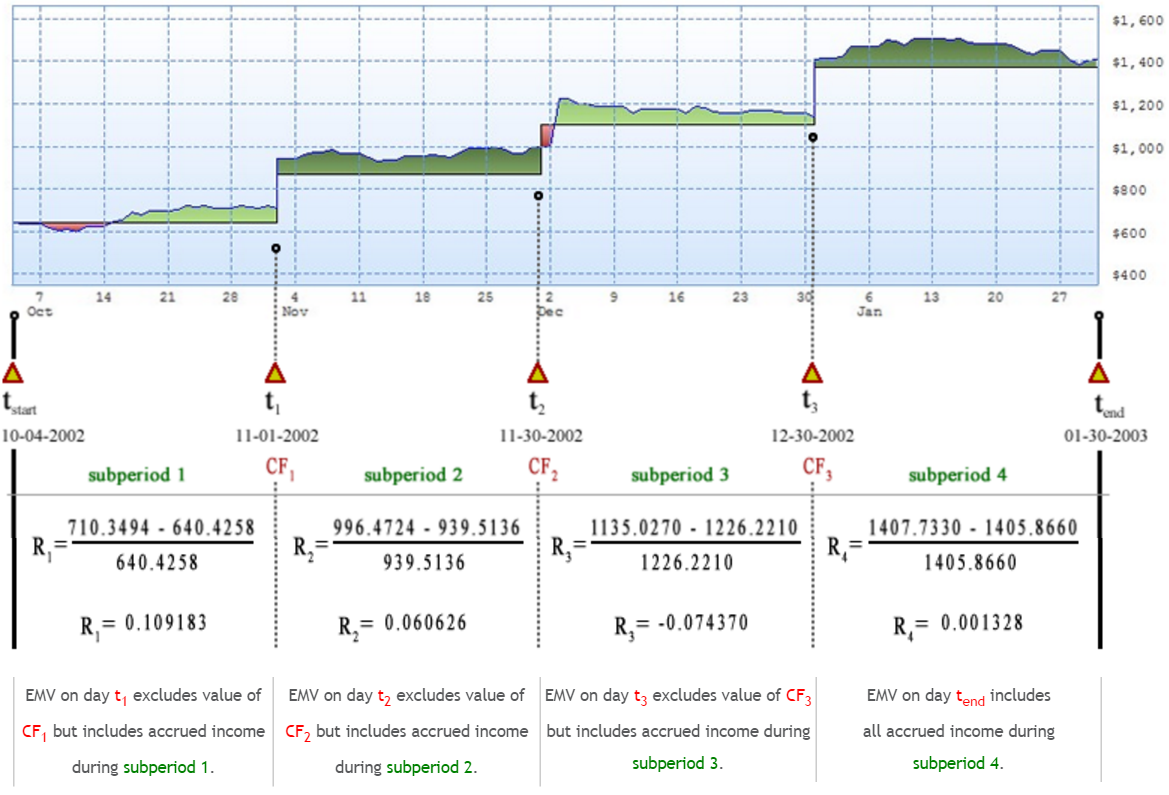

The chart above is a visual representation of transaction history and is known as the Net Investment vs. Market Value chart, by dailyVest. The black line shows the timing and magnitude of each inflow while the blue line shows the market value of that activity.

Please note that this period (10/04/2002 through 01/30/2003) is somewhat of a 'non-standard' period however its frequency of cashflows will help illustrate how to apply the time weighted rate of return, daily valuation method. Typical standard periods are monthly, quarterly, yearly, and multi-year (annualized) periods.

2. Daily Valuation

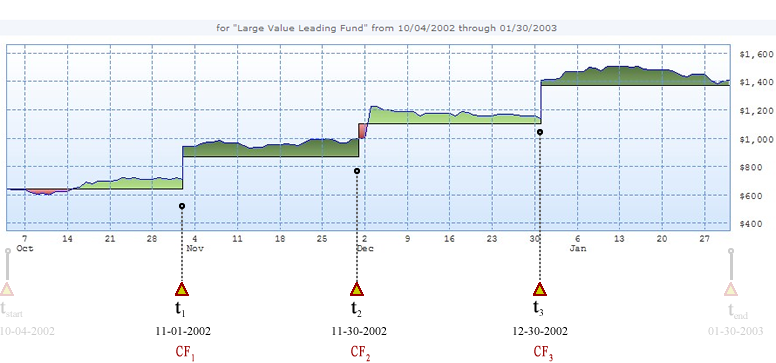

Valuation of all holdings within the account each time there is an external cash flow will result in the most accurate time-weighted rate of return (TWRR) calculation. Daily Valuation breaks the total performance period, 10/04/2002 - 01/30/2003 (see yellow markers) into sub-periods, the boundaries of which are the dates of each cash flow. The formula for calculating a sub-period return is quite simply, this: Rsubperiod = (EMV - BMV)/BMV.

In general, EMV is the market value of the portfolio at the end of the sub-period, before any cash flows in the period, but including accrued income for the period. BMV is the market value at the end of the previous sub-period (i.e., the beginning of the current sub-period), including any cash flows at the end of the previous sub-period and including accrued income up to the end of the previous period.

| Date | Units | Price | Value | |

|---|---|---|---|---|

| BMVtstart | 10/04/2002 | 46.307 | $13.83 | $640.4258 |

| EMVtend | 01/30/2003 | 93.351 | $15.08 | $1,407.7330 |

3. Subperiods marked by cashflows

To start, we must value the holding on days when cashflows CF occur. In this scenario, CF1 occurs on t1 = 11/01/2002, CF2 occurs on t2 = 11/30/2002, and CF3 on t3 = 12/30/2002 as shown by the additional yellow markers below.

Reviewing the transaction information for this scenario will help us determine the BMVs and EMVs and therefore each sub-period return.

| Date | Type | Units | Name | Price | Amount | Unit Balance |

|---|---|---|---|---|---|---|

| 11/01/2002 | Contribution | 14.939 | Large Value Fund | $15.34 | $229.17 | 61.246 |

| 11/30/2002 | Contribution | 14.121 | Large Value Fund | $16.27 | $229.17 | 75.367 |

| 12/30/2002 | Contribution | 17.984 | Large Value Fund | $15.06 | $270.83 | 93.351 |

4. Calculating subperiod returns

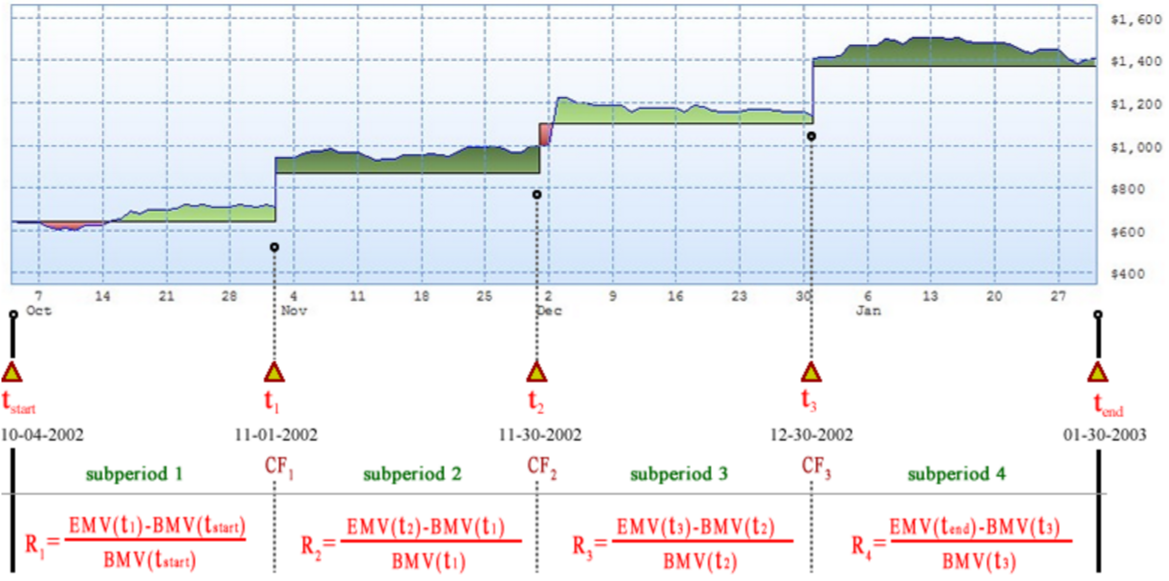

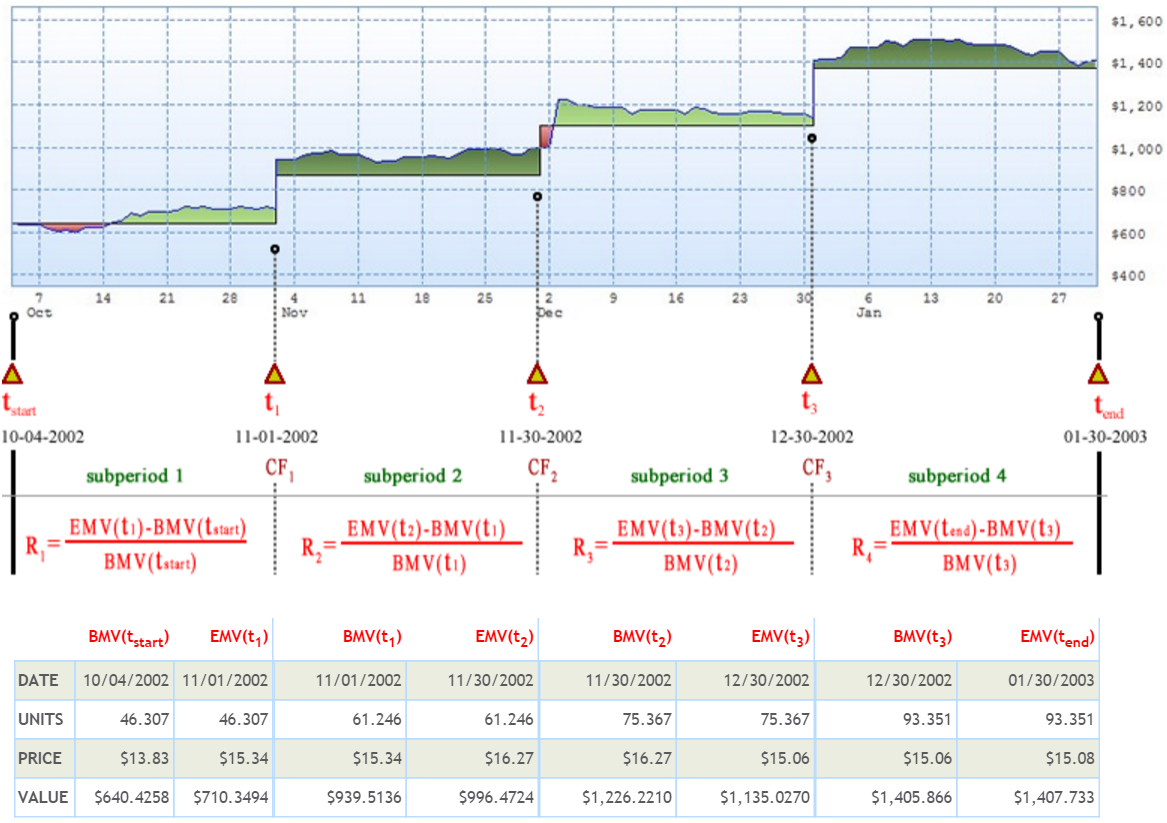

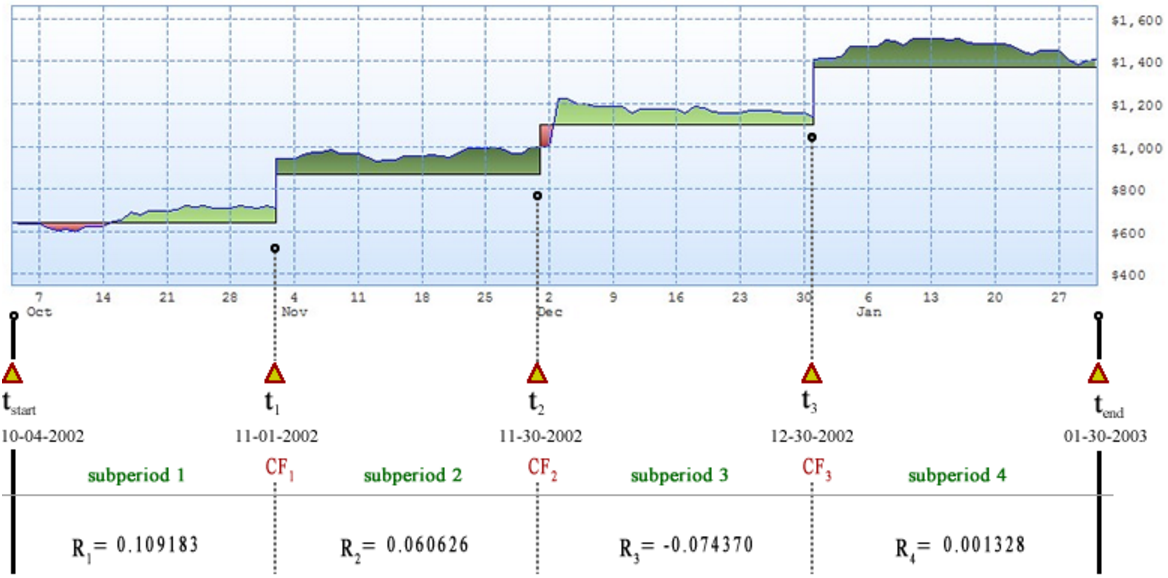

Next we show subperiods 1 - 4 bounded by tstart, the cashflow dates t1, t2, t3, and tend (see all red/yellow triangle markers). With this we can construct our returns for each subperiod using the formula Rsubperiod = (EMV - BMV)/BMV.

In the subperiod return formulas above, we must make sure the EMVs for this holding are before any cash flows in the period, but include accrued income, if any, for that period. Simarlarly, the BMVs at the end of the previous sub-period (i.e., the beginning of the current sub-period) should include any cash flows at the end of the previous sub-period but include accrued income up to the end of the previous period. In the slides ahead we will highlight these points for each subperiod EMV and BMV.

5. Determine BMVs and EMVs

On tstart, t1, t2, t3, and tend we determine the value of the holding by multiplying the number of units or shares at the close times the price. The tables below show how we calculate BMVs and EMVs using price and units for each subperiod. Note that the EMVs on each cashflow day exclude the value of that cashflow but include all accrued income during that subperiod.

6. Subperiod returns calculated. Now what?

In this step we substituted our calculated values of EMV and BMV into each subperiod return formula and performed the calculations as shown below. The final step necessary will be to perform 'geometric linking' on these subperiod returns.

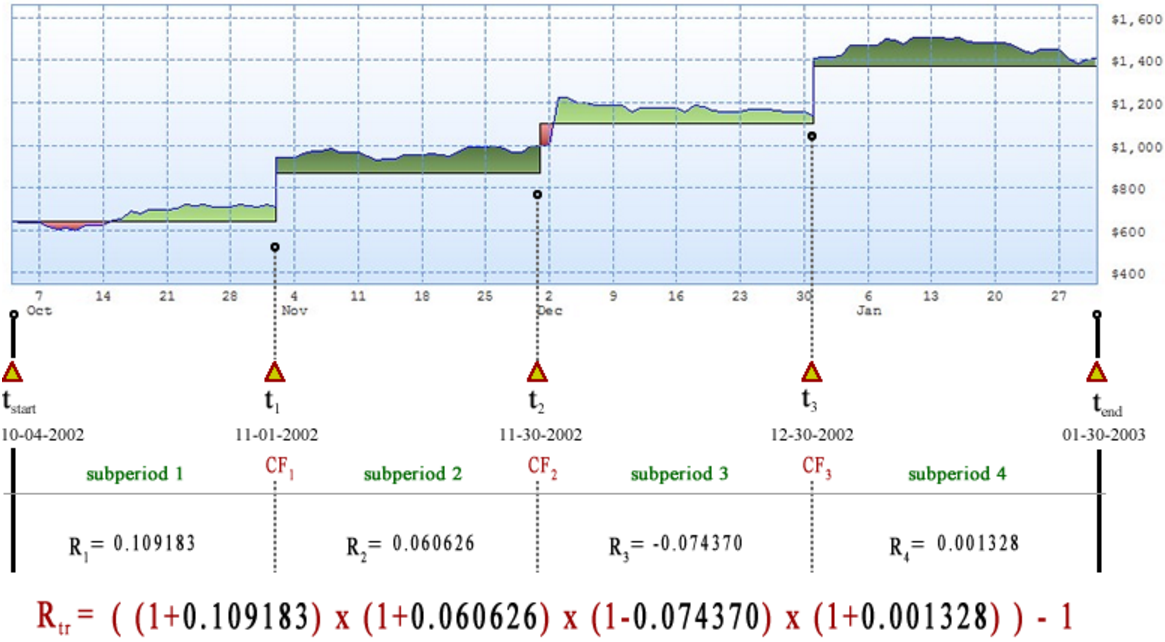

7. Geometric Linking

Geometric linking is a process which must be applied to combine subperiod returns when calculating Total Returns for the Daily Valuation method, as shown here...

8. Evaluate with subperiod returns

In this almost final step, we use the geometric linking equation mentioned above and evaluate it with our calculated subperiod returns R1 - R4...

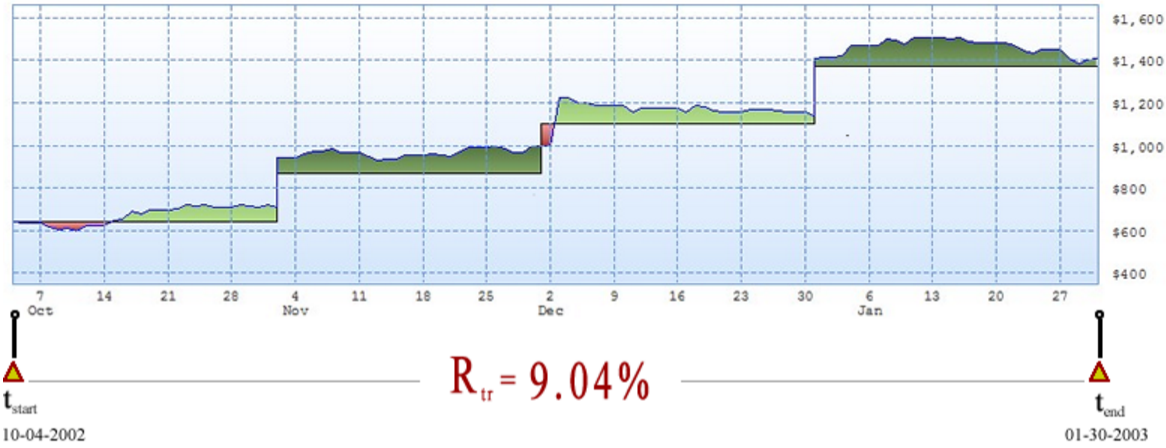

9. Finished! And the answer is?

And the answer is Rtrdailyvaluation = 9.04%. This is the total return for the 'Large Value Fund' over the period 10/04/2002 - 01/30/2003 using the time-Weighted rate of return, daily valuation method.

Finished!!!